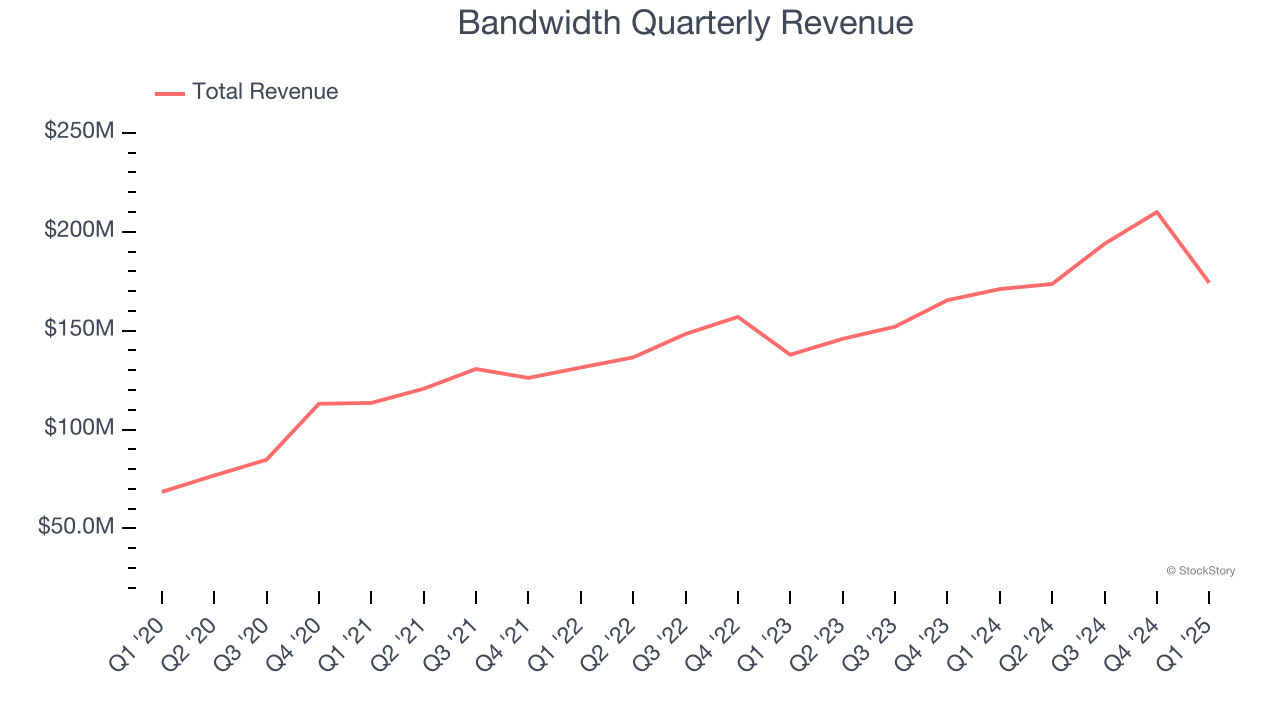

Communications platform-as-a-service company Bandwidth (NASDAQ: BAND) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 1.9% year on year to $174.2 million. Guidance for next quarter’s revenue was better than expected at $179 million at the midpoint, 1% above analysts’ estimates. Its non-GAAP profit of $0.36 per share was 33.3% above analysts’ consensus estimates.

Is now the time to buy Bandwidth? Find out by accessing our full research report, it’s free.

Bandwidth (BAND) Q1 CY2025 Highlights:

- Revenue: $174.2 million vs analyst estimates of $168.9 million (1.9% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0.36 vs analyst estimates of $0.27 (33.3% beat)

- Adjusted Operating Income: -$3.74 million vs analyst estimates of $11.96 million (-2.1% margin, significant miss)

- The company slightly lifted its revenue guidance for the full year to $752.5 million at the midpoint from $750 million

- EBITDA guidance for the full year is $87.5 million at the midpoint, above analyst estimates of $86.38 million

- Operating Margin: -2.7%, up from -6.1% in the same quarter last year

- Free Cash Flow was -$13.3 million, down from $30.35 million in the previous quarter

- Market Capitalization: $364.9 million

Company Overview

Started in 1999 by David Morken who was later joined by Henry Kaestner as co-founder in 2001, Bandwidth (NASDAQ:BAND) provides thousands of customers with a software platform that uses its own global network to provide phone numbers, voice, and text connectivity.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Bandwidth grew its sales at a 13.9% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, Bandwidth reported modest year-on-year revenue growth of 1.9% but beat Wall Street’s estimates by 3.1%. Company management is currently guiding for a 3.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

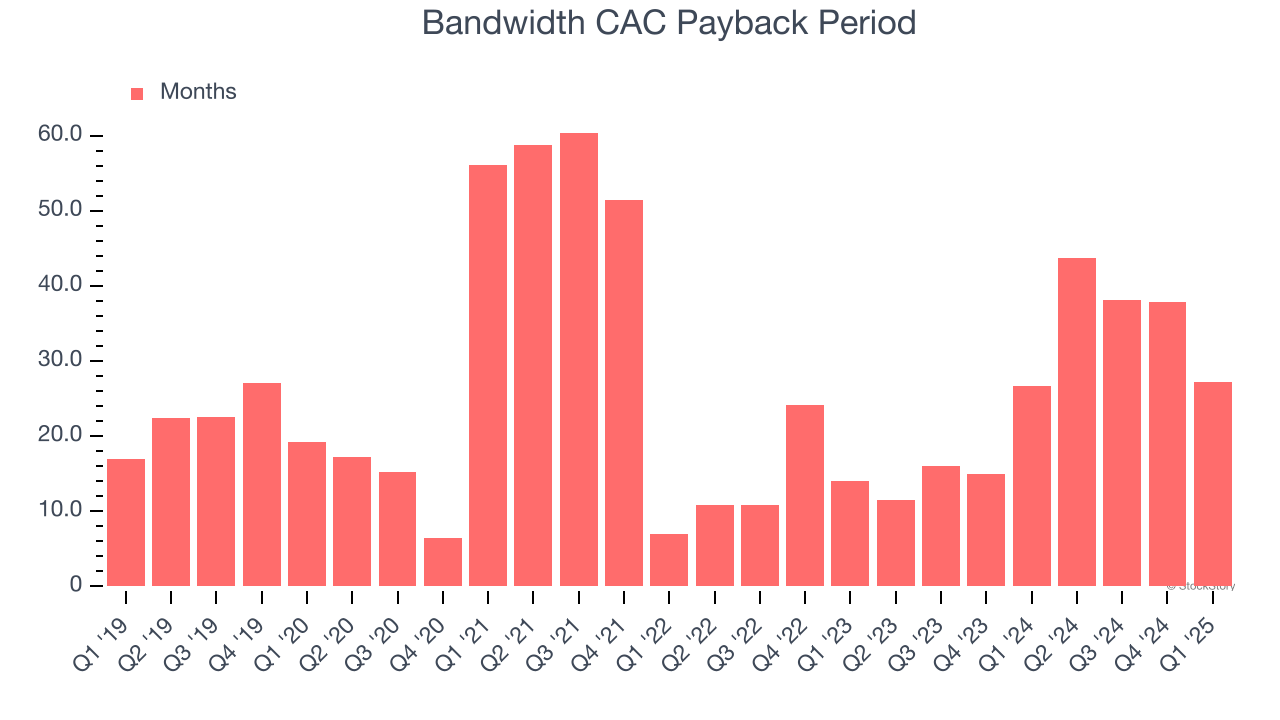

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Bandwidth is very efficient at acquiring new customers, and its CAC payback period checked in at 27.3 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from Bandwidth’s Q1 Results

We were impressed by how Bandwidth blew past analysts’ revenue and EBITDA expectations this quarter. We were also glad it lifted its full-year revenue guidance. On the other hand, its EBITDA missed. Overall, this print had some key positives. The stock traded up 7.7% to $13.24 immediately following the results.

Bandwidth put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.